The global pharmaceutical sector entered the New Year with great gusto. Celgene snapped up Impact Biomedicines for about $7 billion and soon after announced the $9 billion acquisition of Juno Therapeutics. Sanofi acquired Bioverativ for $11.5 billion and then trumped Novo Nordisk to acquire Ablynx for $4.8 billion. The latest, Takeda looking to buy Shire for over $60 billion, would be the biggest deal so far. Big premiums are at play too – Sanofi paid more than 60% premium for Bioverativ and over 100% for Ablynx, while Celgene paid over 90% premium for Juno.

We look at the top pharma deals of this year to understand the stories playing out in the sector.

-

Failure to refuel the top-line through internal assets is leading to an M&A frenzy

Patent cliff is an old story and the sector should have got over it by now; after all, it relies on continuous innovation and scientific breakthrough. However, that hasn’t happened – many pharmas have failed to match the pace needed to replace the loss of sales from the generic erosion. In effect, companies are resorting to M&A in order to recover, diversify, scale up, or slim down.

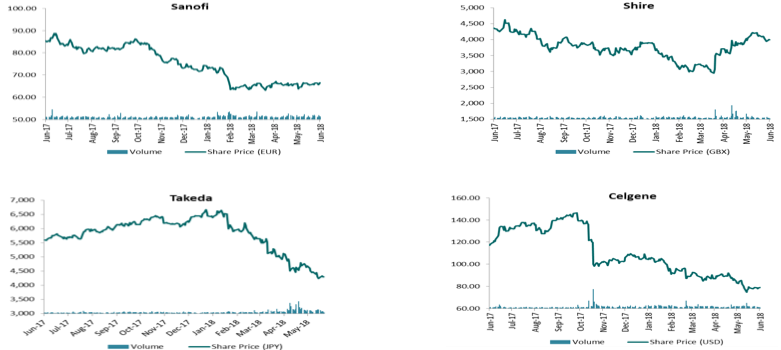

– Takeda/Shire –Takeda’s biggest weakness is the home-market, Japan, with strangulating government policies on pricing, and an increasing onslaught of the generics. Shire offers it a smooth diversification into the US as well as the rare diseases.

– Sanofi – Sanofi lost the patent for its multi-blockbuster diabetes drug Lantus in 2015. Currently, the company is a colossus with clay feet – its diabetes and mature drugs are drying up; the multiple sclerosis franchise is slowing down; cholesterol drug Praluent (launched with a lot of pomp) is barely surviving; the dengue vaccine (again launched with sky-high expectations) was kicked out of The Philippines recently; and the pipeline is scanty. Not a healthy position to be in, with most of the quality drugs/pipeline being in partnership (with Regeneron). The company’s pharma sales in 2017 declined by ~1% YOY, with diabetes declining by 11% YOY globally (-22.8% YOY in the US) and the mature portfolio by 6.4% YOY. Its five-year share price chart reverberates all of these fears.

– Celgene – Celgene has suffered a string of high-profile R&D disappointments in the last couple of quarters, which doesn’t bode well for a company expected to face generic competition for its bestseller, Revlimid, in a couple of years. The Juno and Impax acquisitions provide renewed hopes.

The operational struggles are visible in these pharma companies’ share prices

Source – Thomson Reuters Eikon

-

Blood and genes prevail, while NASH goes out of favour

Smaller companies with specialist drugs in rare diseases have emerged as winners in the M&A race so far. Novartis’s deals with AveXis (acquired for $8.7 billion) and Spark Therapeutics focus on gene therapy. Both of Sanofi’s targets specialise in blood disorders, while Celgene-acquired firms are focused on a rare form of bone marrow cancer and a high-potential gene therapy, CAR-T. Shire too is a rare disease specialist. Due to a huge unmet demand for the treatment of life-threatening diseases, which have a relatively small patient pool, rare diseases offer favourable regulatory terms, premium pricing and consequently higher margins. According to EvaluatePharma’s 2018 report, this space is forecast to grow at a CAGR of 11.4% during 2018-24 vs 6.4% for the overall pharma market.

On the contrary, deals have slowed down in the NASH (Non-Alcoholic Steatohepatitis) space, which saw heightened activity in 2016-17, when Novartis, Allergan, Gilead Sciences and Merck jumped to capture a share of this high-potential market, worth over $20 billion. Perhaps the players are now pulling back to digest these acquisitions, but it is also likely that the space will pull investors back in again over the coming months.

-

The tax money has gone elsewhere

The tax reform in the US was anticipated to be one of the biggest triggers to reignite the M&A frenzy in the sector. The cut in the corporate tax rate, leaving big pharmas with a huge pile of repatriated cash, however, has not done this so far. Of the top 10 companies holding over $150 billion of cash overseas at the end of Q3 2017, the majority have preferred buybacks, while some have started ploughing the money into their R&D labs. According to some sources, the five US pharmas—Pfizer, Merck, AbbVie, Amgen and Celgene—have announced share buybacks worth $45 billion, while ~$23 billion has been spent on US capital projects and R&D. It is surprising to some extent, given the need, so likely that we will see the windfall being used towards M&A.

What to expect next?

The pace of deal-making has slowed down – valuations of the innovative pharmas, especially the biotechs, are still high (although down from the 2015 peaks), while the future of generics/OTCs/consumer health are underwhelming. Novo Nordisk’s empty hands, despite conscientious efforts, and Pfizer’s inability to sell its consumer health business, even after quarters of being on the block, are classic examples. However, the need for strategic acquisitions to plug the revenue gap remains high. For example, Novo Nordisk needs external assets to strengthen its position in the non-diabetes space, in the face of the excruciatingly challenging environment in the diabetes space, and Sanofi still has ~$8 billion left from the budgeted ~$23 billion for acquisitions, while companies including Sanofi, Novartis and Pfizer have been on the lookout for buyers for their non-cores.

Although it is unlikely that 2018 will break records, we should see deal activity coming back to life again after a dull second quarter, as the sector braces up for the next patent cliff (this time from biosimilars). Niches such as rare diseases, oncology and NASH appear to be the favourite areas. The shareholders of such smaller and specialised pharmas should continue to be rewarded for their faith and patience.